Data-driven economic recovery?

This post is a brain dump of my thoughts based on conversations over the last six weeks.

Call to action: formally convene and coordinate our collective intelligence to accelerate development on the challenges we see—and achieve better outcomes faster.

My understanding is that around the world, people are struggling to model the economic and social impacts of the pandemic. There’s a lot going on with health data, but not much elsewhere.

In the age of ‘big data’ we should be able to derive what is going on from our measured reality, not (just) models. Most of finance is already ‘digital’.

In the UK, most small businesses have under one month of available cash-flow and banks, even with 80% government backing, are not lending to most (we’ll see how today’s announcement of 100% backing changes this).

So far less than 2% of available C-BILS are deployed.

This means at the end of this week, if they have not already, we’d expect a vast swathe of businesses to be effectively bankrupt. Lockdown isn’t going to end soon: there is no rapid reboot curve in any scenario. This is awful for millions of people.

How might we help decision-makers with faster, better insights?

Many people need better insights into economic systems impacts, not just Treasury. It is a federated challenge in terms of both supply and demand. It needs a federated set of solutions — data increases in value the more it is connected.

By bringing people together across the financial system (banks, fintechs, accounting software, credit agencies, businesses, etc) and public sector (treasuries, regulators, data protection, central banks) we could build on the principles of shared data, open banking and related initiatives, to create a process for continuous assessment of both businesses and individuals, based on real data.

Continuous assessment could help identify who are the most at-risk, what interventions are needed and when.

We could automate interventions rather than wait for people to have to apply.

For example, it is possible that the following collection of information could be analysed on a daily basis:

- Every transaction (payments and receipts) in all bank accounts

- Every creditor and debtor (including payroll) in accounting packages

- All assets and liabilities (in contracts)

With a cohesive aggregated approach to data collection and analysis, we could meet the needs of many decision-makers.

We have digital processes and systems for (1) and (2) but are almost ‘nowhere’ on (3). We also need to note that many small businesses only have (1) as they do not use digital accounting packages.

Digital culture and data skills are needed at all levels in the decision-making chain

We also cannot understate the need for digital and skills to help shape decision-making in a crisis. This applies to all sectors and territories.

Data governance needs to be a foundation if we are to expect good outcomes.

There are very high barriers to data sharing, but we have got the tools, skills and processes to deal with the challenges.

Unfortunately, they are not widely distributed: we need training and support packages that will aid ministers, civil servants, business leaders, analysts and developers through this minefield.

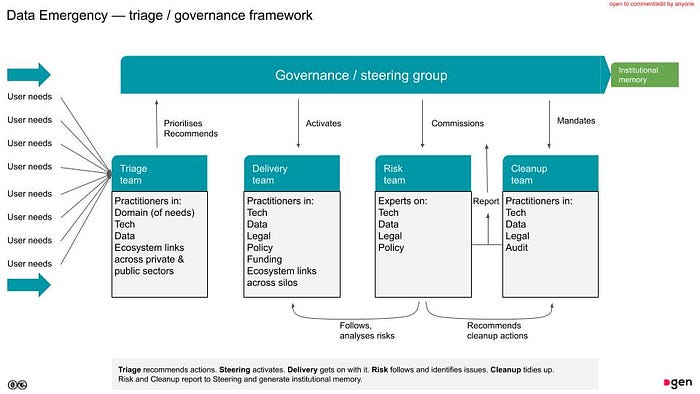

In the ‘rush to solutionise’ from many in the development community, I found myself creating a ‘101 for data triage’ to help people try and pause and think through what the user-needs really might be (who needed what insight in which format and frequency). What skills might be required? (including legal, policy, software and analytics)? What’s the development process to develop and test potential analysis and interventions.

It has made me wonder:

Perhaps we should have a SAGE for data governance?

I’m very lucky to be connected with many domain experts in this space and to have run many data-driven initiatives. Having such visibility also carries a responsibility to call out that I think we could do much better than we are today: where we need to support the people at the ‘data frontline’ accelerate their efforts with the right ‘air cover’ of skills and leadership. We need to do it now and get as many people to the table as possible.

There are some fantastic people across organisations working on this (including HM Treasury, Bank of England, ICO, OBIE, GOFCoE, FDATA, and BEIS to name but a few in the UK). More broadly countries like New Zealand are bringing to bear their substantial experience and benefitting from a ‘smaller’ ecosystem which must be convened. Global organisations are finding themselves challenged with the lack of embedded digital skills and the usual playbooks may look ok on paper, but don’t match the reality on the ground in the countries they are trying to support.

I think we need to do more to both make the most of what we have while protecting the data rights of both businesses and consumers.

We have a duty of care to perform on this, both nationally and, given our specific domain experiences in financial data, to help internationally — especially in countries that have no, or little, data infrastructure.

And, if we crack any of this, how can we use it all to create a wealth of outcomes, rather than just outcomes of wealth?